Disability Insurance

There are a lot of factors involved with each opportunity, and because of the complexity, DI quotes can’t be run online. We’ll create an illustration tailored to your client, then give you the product-specific ideas and sales support to help secure the deal. You can start by giving us a call or filling out a quote request form.

The process of determining if your client will qualify for disability insurance is called underwriting. Underwriting for DI is different than life insurance underwriting, since DI coverage protects against the risk of morbidity, while life insurance uses mortality data to assess the likelihood of death.

Disability insurance carriers exclude certain occupations from coverage, but eligibility is primarily based on the information you can provide about your client. This process is called field underwriting — your initial data gathering before any quotes are run. The more our team knows, the better we can determine if your client will qualify. Some key factors include:

- Occupation with specific daily duties

- Date of birth, height and weight

- State of residence

- Tobacco user status

- Any medical issues, including back or heart trouble, sleep apnea, stress, anxiety, depression, etc.

- Income/business information

- Employees: W2 income

- Business Owner: Net taxable reportable income, how long they have owned the business and how many employees they have

If you need help asking the right questions, our DI Quote Request form is a good place to start, or you can call our team to talk through your client’s eligibility.

Insurance companies define disability in one of three ways: Total, residual or catastrophic. See below for an explanation of each potential situation. You don’t have to be totally disabled and unable to work – you can potentially go back to work or get a different job while receiving benefits.

Total Disability

Your Occupation: Unable to perform substantial and material duties of your occupation and not working in any occupation

Regular Occupation: Totally disabled from regular occupation and choosing to work in another occupation; benefits are provided regardless of income earned from other occupation

Transitional Occupation: Unable to perform substantial and material duties of regular occupation, but working in another occupation; benefits are based on replacement of pre-disability earnings up to 100 percent

Residual Disability

Elects to work in another occupation, return to work full-time or work at a reduced capacity in “your occupation” and have a loss of earnings; benefits are proportionate to the loss of earnings

Catastrophic Disability

Cannot perform two or more of the Activities of Daily Living: bathing, continence, dressing, eating/feeding, toileting or transferring; or is cognitively impaired or presumptively disabled

This is a critical aspect for DI underwriting. For W2 you'll need last year’s W2 and a recent pay stub. For business owners, you'll need the last two years of tax returns with all schedules. We'll serve as your client’s advocate with insurance company underwriters.

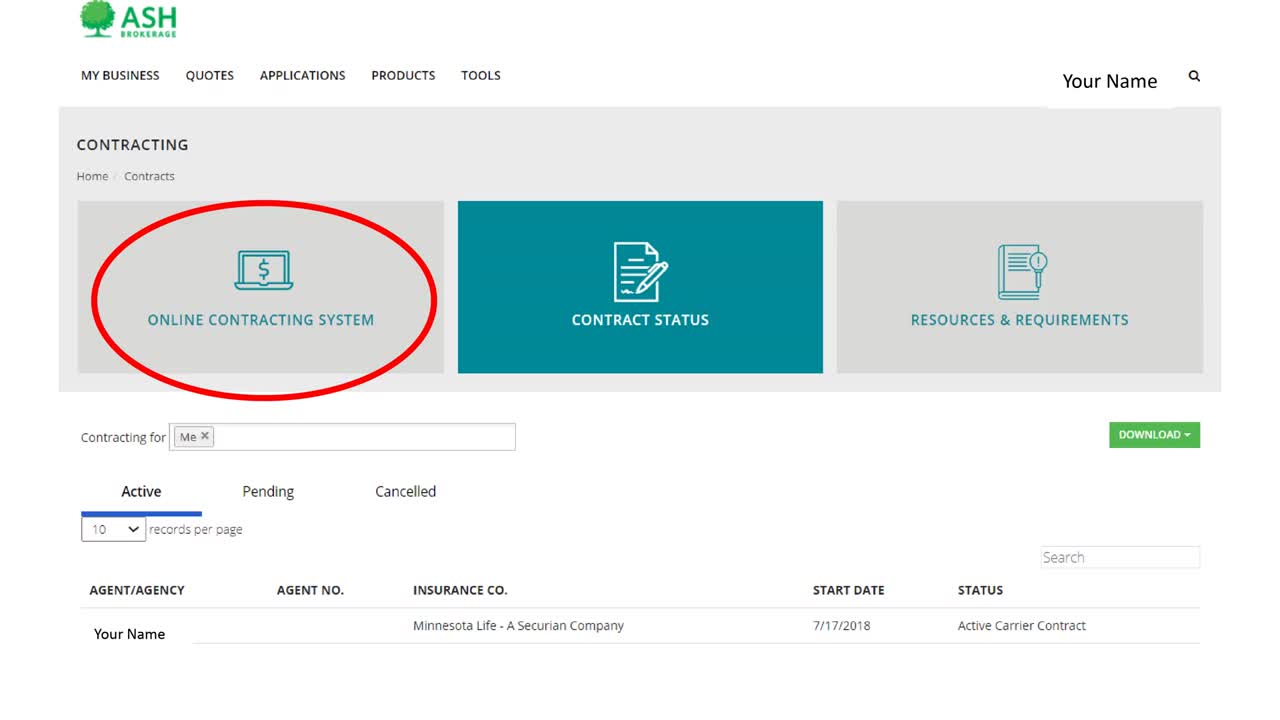

Everything is done online through an electronic contracting system called SureLC. You'll want to log in to the Advisor Portal. From the homepage, click on the Contracting tile, then choose Online Contracting.

For the initial setup, your information pulls directly from the National Insurance Producer Registry – it may be as easy as verifying no changes are needed or completing your profile that includes submitting your signature card, Errors and Omission coverage, AML, and if directly paid, direct deposit information.

After setting up your initial profile with our online contracting system, you can request additional insurance carrier contracts at the click of a button. You can also update any contracting documents such as AML, E&O, or bank information. No more unnecessary duplication of efforts, redundant questions or searching for up-to-date paperwork. It’s fast, paper-free, and it’s always available when you need it.

If you need help, our Commissions and Contracting team is available to make sure the insurance process never stands in the way of progress.

Ash Brokerage has a range of solutions available to meet your clients’ needs. Our carriers have white-collar, middle America or special/impaired risk focuses:

- For white collar, Petersen International, Principal and The Standard

- For middle America, Assurity, Illinois Mutual and Mutual of Omaha

- For blue collar, Assurity, Fidelity and Petersen International

Clients receive benefits after incurring a qualifying disability and satisfying the policy’s waiting period, often referred to as an elimination period. As a rule, the shorter the elimination period, the more expensive a policy will be. It’s important for clients to understand that benefits are typically not paid until the end of the month following the elimination period.

- Most people choose either a 90-day or 180-day elimination period

- Clients will want to consider their available savings and assets when making this choice

The answer is twofold. First, when clients are disabled, the benefit period is the length of time they’re paid. The shortest option is two years, but the most common benefit period is five years. Second, their policy will have an age limit – most people purchase coverage that lasts until age 65.

- Clients should buy a policy with the longest benefit period they can afford

- Coverage may be adjusted for a longer benefit period in the future; additional underwriting may be needed

Benefits are based on a percentage of your client’s income. The maximum amount depends on a variety of factors, such as current income, occupation and existing coverage.

Policies can be designed to meet most needs and budgets – from maximum income protection to safeguarding specific expenses, such as a mortgage. Typically, premium costs between 1 and 3 percent of the client’s annual income.